最大的合法配资平台 我们认为反导工业(纽交所:ABM)正在冒一些债务风险

发布日期:2024-11-05 21:11 点击次数:140

其中,陶诚放弃的基本薪酬为48万元,效益年薪为8万元至64万元(具体以年度考核结果为准),合计为56万元至112万元;张贤明放弃的基本薪酬为36万元,效益年薪为6万元至18万元(具体以年度考核结果为准)最大的合法配资平台,合计为42万元至54万元。

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies ABM Industries Incorporated (NYSE:ABM) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

How Much Debt Does ABM Industries Carry?

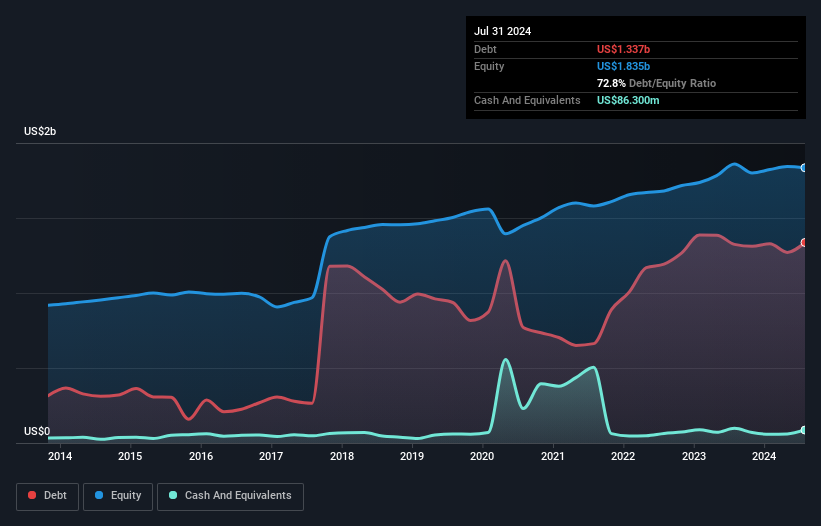

As you can see below, ABM Industries had US$1.34b of debt, at July 2024, which is about the same as the year before. You can click the chart for greater detail. However, it also had US$86.3m in cash, and so its net debt is US$1.25b.

NYSE:ABM Debt to Equity History October 7th 2024

How Healthy Is ABM Industries' Balance Sheet?

]article_adlist-->

WecanseefromthemostrecentbalancesheetthatABMIndustrieshadliabilitiesofUS$1.25bfallingduewithinayear,andliabilitiesofUS$1.96bduebeyondthat.Ontheotherhand,ithadcashofUS$86.3mandUS$1.48bworthofreceivablesduewithinayear.SoithasliabilitiestotallingUS$1.64bmorethanitscashandnear-termreceivables,combined.

This deficit isn't so bad because ABM Industries is worth US$3.22b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

ABM Industries's debt is 3.4 times its EBITDA, and its EBIT cover its interest expense 3.1 times over. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Investors should also be troubled by the fact that ABM Industries saw its EBIT drop by 17% over the last twelve months. If that's the way things keep going handling the debt load will be like delivering hot coffees on a pogo stick. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine ABM Industries's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, ABM Industries's free cash flow amounted to 40% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

Mulling over ABM Industries's attempt at (not) growing its EBIT, we're certainly not enthusiastic. Having said that, its ability to convert EBIT to free cash flow isn't such a worry. Looking at the bigger picture, it seems clear to us that ABM Industries's use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 3 warning signs with ABM Industries , and understanding them should be part of your investment process.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock最大的合法配资平台, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

海量资讯、精准解读,尽在新浪财经APP

海量资讯、精准解读,尽在新浪财经APP